In a world where money is increasingly digital yet fundamentally fragile, Bitcoin offers something that sounds almost paradoxical: a digital asset with no issuer, no headquarters, and no CEO that nevertheless maintains unwavering scarcity and operates without interruption. To understand why this matters, it helps to step back and look at what money actually does for us, and where our current systems fall short.

Money serves three essential functions. It must act as a medium of exchange, allowing us to trade without the inefficiency of barter. It must serve as a unit of account, giving us a common language for pricing goods and services. And perhaps most critically, it must function as a store of value, enabling us to defer consumption today in order to consume tomorrow. For money to perform this last function well, people need to trust that it will hold its purchasing power over time.

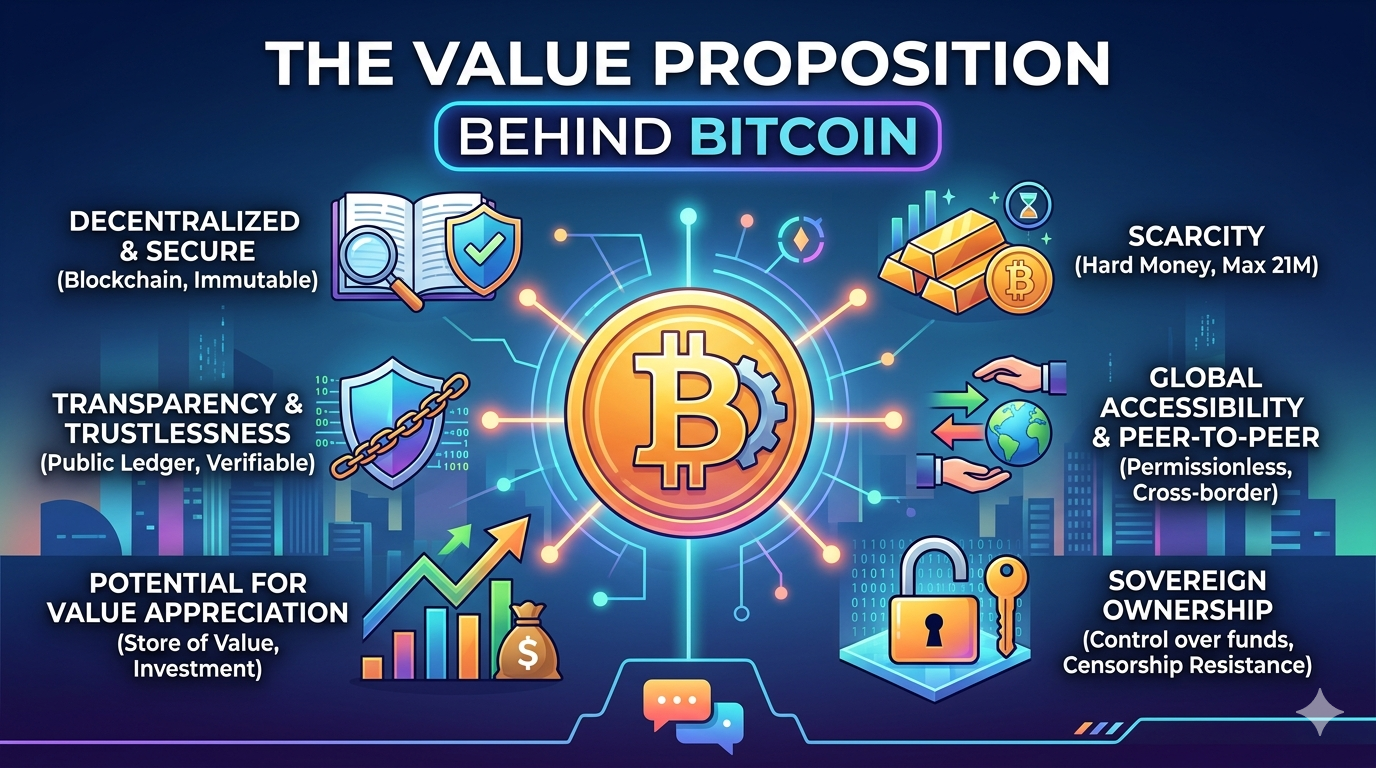

Our modern monetary systems are built on trust in institutions. Central banks manage the supply of currency, adjusting it in response to economic conditions. Commercial banks maintain ledgers of who owns what, and payment networks facilitate the movement of funds across borders. This architecture has delivered tremendous benefits, enabling global commerce and economic growth on a scale previously unimaginable. Yet it also introduces vulnerabilities that have become increasingly apparent.The most fundamental of these vulnerabilities concerns supply. When a central bank faces pressure to stimulate economic activity, manage debt burdens, or respond to crises, the temptation to expand the money supply can become overwhelming. This is not a matter of corruption or incompetence; it is the inherent nature of discretionary monetary policy. Each unit of currency created dilutes the value of those already in circulation. Over decades and centuries, this gradual erosion compounds dramatically. A dollar saved in 1970 has lost the vast majority of its purchasing power today. This is not an accident of history but a predictable consequence of monetary systems with no hard constraints on issuance.

Bitcoin addresses this problem through an elegant mechanism of programmatic scarcity. The protocol specifies that only twenty-one million bitcoins will ever exist, and this limit is enforced not by the promise of any institution but by the consensus rules of the network itself. New bitcoins are issued according to a predetermined schedule that halves approximately every four years, creating a supply curve that asymptotically approaches the cap. No committee can convene to alter this schedule. No emergency decree can override it. The scarcity is not merely promised; it is engineered into the software and secured by the economic incentives of the network’s participants.

This leads to another dimension of Bitcoin’s value proposition: its resistance to censorship and seizure. In traditional financial systems, intermediaries have the technical ability and often the legal obligation to freeze accounts, block transactions, or confiscate funds. These powers serve legitimate purposes in combating crime and enforcing court judgments, but they also create systemic risk. Political pressures, administrative errors, or changes in regulatory posture can suddenly render individuals or organizations unable to access their own wealth. Bitcoin transactions, by contrast, require no permission from any authority. Once broadcast to the network and confirmed, they are extraordinarily difficult to reverse. The private keys that control bitcoin holdings exist solely in the possession of their owners, making arbitrary seizure practically impossible without direct coercion of the individual.

The network’s architecture reinforces these properties through decentralization. Unlike payment systems that rely on central servers or databases, Bitcoin operates across thousands of independently operated nodes distributed globally. Each node maintains a complete copy of the transaction history and verifies every new transaction against the protocol rules. There is no single point of failure that could bring the system down, no database administrator who could alter records, and no corporate board that could change the terms of service. The network has operated continuously since its inception in 2009, processing transactions every ten minutes on average, through financial crises, geopolitical conflicts, and regulatory crackdowns in various jurisdictions.

This resilience comes with trade-offs that are important to acknowledge honestly. Bitcoin’s transaction throughput is modest compared to conventional payment networks. The energy required to secure the network through proof-of-work mining is substantial and has generated legitimate environmental concerns. Price volatility remains significant, making Bitcoin less than ideal as a unit of account in the near term. And the irreversibility of transactions, while protecting against censorship, means that mistakes or theft cannot easily be undone.Yet these limitations do not negate the core value proposition; they merely define its appropriate applications. Bitcoin is not positioned to replace every function of the existing financial system. Rather, it offers a complementary alternative optimized for specific qualities that traditional systems cannot replicate. It functions as a form of digital gold, a settlement layer for high-value transactions, and a savings technology for those who prioritize sovereignty and long-term purchasing power protection over convenience and short-term stability.

The philosophical underpinnings of Bitcoin reflect a particular worldview about the relationship between individuals and institutions. Its creator, operating under the pseudonym Satoshi Nakamoto, embedded a newspaper headline in the very first block of the blockchain: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.” This was not merely a timestamp but a statement of purpose. Bitcoin emerged from the ashes of the global financial crisis as a technological response to the perceived failures of centralized financial architecture. It represents a bet that mathematical rules and economic incentives can provide more reliable monetary foundations than human discretion.

For individuals in countries with unstable currencies or unreliable banking systems, this is not an abstract philosophical position but a practical necessity. Citizens of nations experiencing hyperinflation have watched their life savings evaporate despite their best efforts at financial prudence. Those in jurisdictions with capital controls have found their wealth trapped, unable to move to safer harbors. Political dissidents have seen their accounts frozen for expressing views contrary to those in power. For these populations, Bitcoin offers something beyond speculation: a lifeline to financial participation in the global economy and protection against the arbitrary exercise of state power over money.

Even in stable democracies with functional institutions, the value proposition resonates with those who recognize that trust is not costless. Every layer of financial intermediation introduces counterparty risk. Every institutional promise of stability depends on the continued good judgment of fallible human beings operating under political and economic pressures. Bitcoin offers a hedge against the slow degradation of monetary standards and the possibility of more abrupt systemic failures. It is not a rejection of all institutional trust but a diversification of trust, adding a foundation of cryptographic verification and economic incentive to complement the traditional reliance on human integrity and institutional reputation.

The network effects surrounding Bitcoin reinforce its position. As more individuals, companies, and even nation-states adopt it as a treasury reserve asset or payment mechanism, the utility of holding and using Bitcoin increases. The liquidity deepens, the infrastructure improves, and the regulatory clarity gradually advances. This creates a virtuous cycle where adoption begets further adoption, gradually transforming Bitcoin from an experimental technology into an established component of the global financial landscape.

Ultimately, the value of Bitcoin lies not in any single feature considered in isolation but in the particular combination of properties it achieves simultaneously. It is scarce yet divisible. It is digital yet bearer-based. It is globally accessible yet resistant to centralized control. It is transparent in its operation yet pseudonymous in its use. No other asset or technology has successfully combined these characteristics in quite the same way.

Whether one views Bitcoin as the future of money, a speculative bubble, or something in between, understanding its value proposition requires engaging with the genuine problems it seeks to solve. The erosion of purchasing power through monetary expansion, the vulnerability of wealth held in intermediated form, and the systemic risks of centralized financial architectures are not theoretical concerns but historical realities that repeat across time and geography. Bitcoin offers one possible answer to these challenges, encoded in software and sustained by the collective choice of millions of participants who find value in its unique properties.